Constraint Is Replacing Surprise

Labor, capital discipline, and the cost of time under restriction

This week did not introduce a new macro shock. It clarified where constraints are beginning to bind.

Several long-debated dynamics have moved from theory into observable behavior. Employers are adjusting labor decisions. Investors are responding differently to capital intensity. Governments operating under strain are signaling limits rather than expansion.

These shifts matter because they influence capital allocation without requiring a crisis. They change how long institutions are willing to wait, how risk is priced over time, and which assumptions are quietly being retired.

The goal of this note is not to catalogue events. It is to situate these behavioral changes within a broader macro and institutional context.

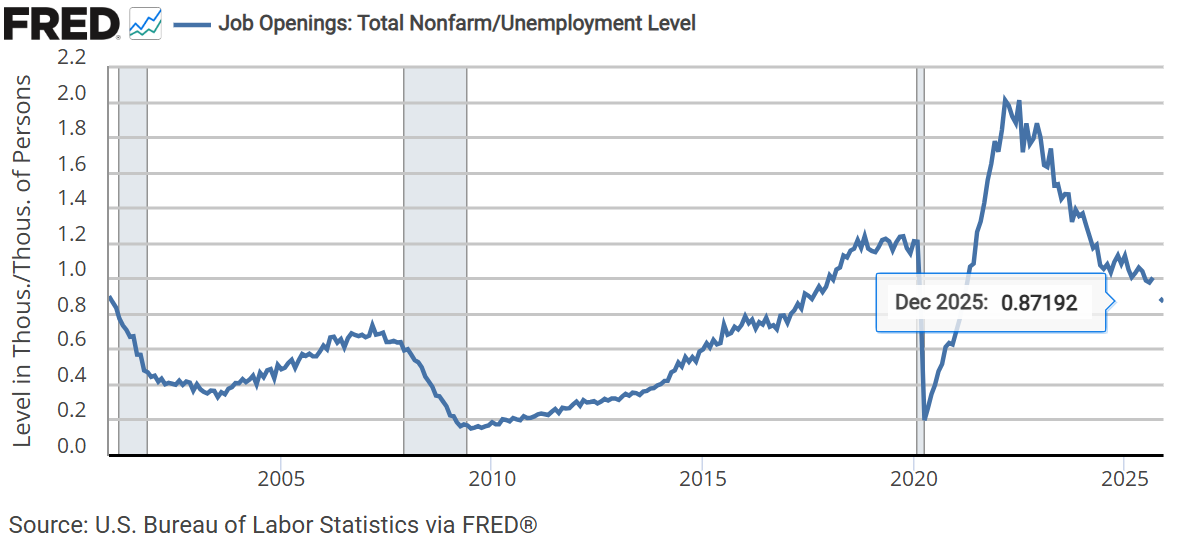

The labor market is no longer absorbing pressure

The most consequential macro development remains the evolution of the U.S. labor market.

Recent data show job openings declining to a level below their pre-pandemic relationship with unemployment. At the same time, announced layoffs have risen meaningfully across private surveys, with confirmation from official releases. Taken together, this reflects a shift in employer posture rather than a temporary fluctuation.

For much of the post-pandemic period, firms prioritized labor retention despite slowing growth and higher costs. That behavior supported wage growth, sustained services inflation, and allowed financial conditions to remain restrictive without immediate employment stress.

That buffer is now thinner.

When firms move from delaying hiring to planning reductions, labor stops acting as a stabilizer. Wage pressure does not collapse quickly, but it becomes asymmetric. Downside pressure builds more easily than upside acceleration. This matters because labor costs are the core input for the services economy, and services remain the dominant driver of underlying inflation.

From a capital allocation perspective, this shift affects margins, pricing power, and demand durability across sectors. It also alters how long restrictive conditions can persist before private behavior adjusts elsewhere.

Time under restriction has become the binding variable

The second signal is less visible but equally important.

The dominant macro constraint is no longer uncertainty about the next policy move. It is the duration of elevated real yields and restrictive financial conditions.

Markets have experienced months of limited progress rather than acute stress. Rates remain high in real terms. Liquidity is present but increasingly selective. This environment produces a different kind of pressure.

Short, sharp drawdowns force rapid repricing and often attract a policy response. Prolonged stagnation does neither. Instead, it quietly alters behavior. Opportunity cost rises. Patience erodes. Decision-makers begin to favor flexibility over expansion and near-term resilience over long-duration commitments.

This dynamic reshapes capital allocation without any formal tightening. Capital-intensive projects face greater scrutiny. Balance sheet optionality becomes more valuable. The tolerance for extended payback periods declines even when long-term narratives remain intact.

The risk here is not an abrupt break. It is gradual disengagement. That process tends to be slower, less visible, and more difficult to reverse once it takes hold.

Capital discipline is being reimposed on large technology

One of the clearest institutional reactions this week came from equity markets.

Large technology firms continue to commit substantial capital to AI infrastructure. What changed was not the scale of investment, but how it was received.

Announcements that would previously have been interpreted as strategic strength were met with sharp equity repricing. The response was not a judgment on the technology itself. It was a reassessment of capital allocation trade-offs.

Sustained capital expenditures reduce flexibility. They compete directly with shareholder returns and balance sheet optionality. They also raise the required return threshold in an environment where competitive differentiation is uncertain and the cost of capital is no longer negligible.

This reaction signals a constraint being enforced by investors. Growth narratives are no longer sufficient on their own. Institutions are beginning to price the cost of capital intensity, not just the promise of innovation.

This matters beyond equities. When capital discipline tightens at the top of the market, it eventually influences credit conditions, merger activity, and investment pacing across the ecosystem.

Private credit is reassessing software exposure

That influence is already visible in credit markets.

Private credit has significant exposure to software and technology-adjacent businesses. Many of these loans were underwritten during a period of low rates, stable growth assumptions, and limited perceived disruption risk.

The emergence of low-cost AI tools capable of replacing certain software functions has introduced uncertainty around long-term cash flow durability. The issue is not immediate displacement. It is gradual erosion of pricing power and switching costs.

Equity markets reacted first, particularly in software names. Credit markets followed by repricing managers with concentrated exposure. This is a forced adjustment rather than a speculative one. When the stability of cash flows becomes less certain, underwriting assumptions must change.

This does not imply imminent stress. It implies tighter standards, greater differentiation, and a reassessment of what constitutes defensive exposure. For institutions that viewed private credit as insulated from public market dynamics, this shift is material.

Fiscal limits are becoming visible in geopolitics

Away from U.S. markets, one structural constraint deserves attention.

Russia has sustained elevated war-related spending through a combination of higher domestic taxes, reserve asset liquidation, and a significant expansion of bank credit. Revenue growth, particularly from energy, has slowed. Deficits have widened in real terms.

Recent official data indicate that this approach is reaching its practical limit. Planned spending growth is slowing. Military and security outlays are expected to remain flat in nominal terms next year. These are not signals of strategic retreat. They are signals of constraint.

For capital markets, the relevance lies in capacity rather than outcome. Fiscal strain shapes geopolitical bargaining positions, energy supply decisions, and the durability of sanctions regimes. It also increases the linkage between fiscal policy and domestic financial stability.

Constraints matter even when objectives remain unchanged.

What to pay attention to next week

The coming week does not require new narratives. It requires attention to follow-through.

Watch whether labor data continue to reflect employer behavior rather than sentiment. Consistency across releases matters more than any single print.

Observe how markets respond to further disclosures around capital spending. The reaction function is evolving, and that evolution carries more information than the announcements themselves.

Listen closely to credit commentary, particularly around underwriting standards and sector exposure. Language often shifts before pricing does.

Finally, note whether policy communication acknowledges time as a constraint rather than a neutral variable. When that recognition appears, it usually arrives quietly.

The signals this week were not dramatic. They were persistent. That is often how conditions change.